The CSRD and ESRS are closely linked. The CSRD Directive specifies which companies are required to report and when this requirement takes effect. The ESRS standards, on the other hand, specify what information must be disclosed and how it should be prepared.

Recently, the regulations governing sustainability reporting have undergone significant changes. These changes affected both the timeline for the implementation of these obligations and the scope of entities subject to reporting, as well as the ESRS standards themselves. The most important changes were related to the package Omnibus I, including the „stop the clock” directive, Directive 2026/470, and work on simplified ESRS.

The most important changes will be discussed later in this article.

The CSRD, or Corporate Sustainability Reporting Directive, is Directive (EU) 2022/2464 of the European Parliament and of the Council of December 14, 2022. It amended several earlier legal acts, including Regulation (EU) No. 537/2014, Directive 2004/109/EC, Directive 2006/43/EC, and Directive 2013/34/EU, with regard to corporate sustainability reporting.

The directive was adopted by the European Parliament and the Council in the fall of 2022, then published in the Official Journal of the European Union, and entered into force twenty days after its publication.

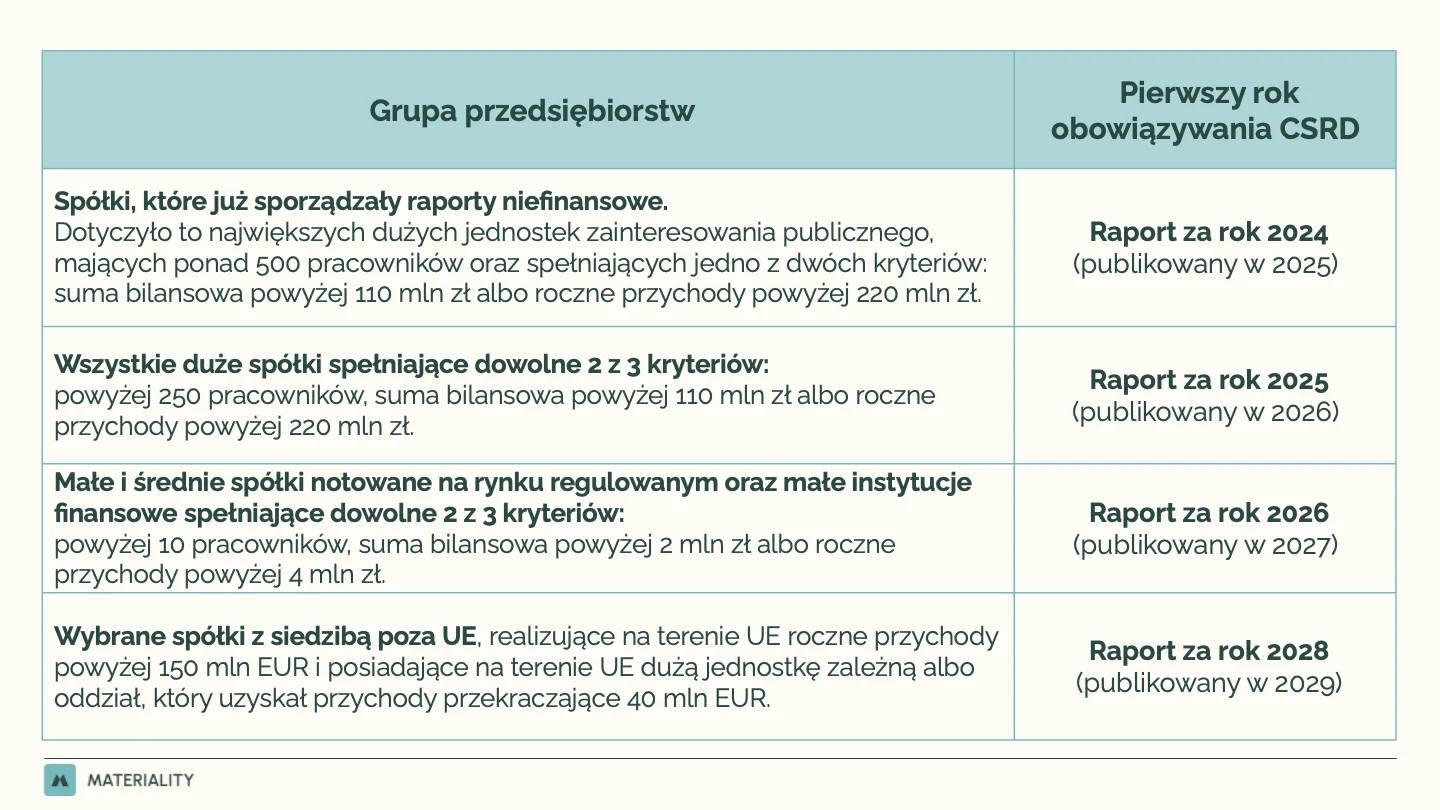

The CSRD has introduced, at the European Union level, a requirement to report information on sustainability in accordance with the uniform European Sustainability Reporting Standards (ESRS). According to the original plan, the reporting requirements were to be phased in for additional groups of companies, starting with reporting for the year 2024.

The current scope of obligations under the CSRD is the result of several stages of legislative changes. The starting point was the original version of the directive, which provided for a broad scope of companies subject to reporting requirements. Subsequently, as part of the package Omnibus I, solutions were proposed that would result in the postponement of some deadlines and a narrowing of the scope of entities subject to mandatory reporting. To understand the current requirements, it is therefore important to review both the original provisions of the directive and the subsequent amendments introduced during the various stages of the legislative process.

In its original version, the CSRD directive provided for a significant expansion of the non-financial reporting obligations previously in force under the IFRS Directive.

The starting point was the recognition that previous regulations did not provide sufficiently comparable, reliable, and complete information on sustainable development, despite the growing demand for such data from investors, financial institutions, business partners, and other stakeholders. The CSRD was therefore intended not only to expand the scope of reporting to include a greater number of entities but also to improve the quality, consistency, and usefulness of the disclosed information through the harmonized ESRS reporting standards.

The original CSRD model called for the phased extension of reporting requirements to successive groups of companies, starting with the largest public-interest entities that had previously been subject to non-financial reporting, through the extension of the requirement to all large companies, both listed and unlisted, and ultimately to include listed small and medium-sized enterprises, as well as certain entities based outside the European Union.

A significant change introduced by the CSRD also concerned the very nature of reporting. It replaced an approach based on more general non-financial disclosures with a model based on uniform European sustainability reporting standards (ESRS). The CSRD and the ESRS standards base reporting on the principle of double materiality, according to which a company should analyze and disclose information from two perspectives. The first concerns the impact of the company’s operations on people and the environment, and the second concerns the impact of sustainability issues on the company itself, its development, performance, financial position, business model, strategy, and risks. This approach was intended to increase the usefulness of reporting for various audiences, including investors, financial institutions, business partners, employees, civil society organizations, and other stakeholders who need both information about risks to the company and information about the impacts of its operations on people and the environment. The CSRD also provided for strengthening the credibility of reporting through the requirement to have sustainability reports attested. The original version of the directive assumed that, initially, the assurance would be at the level of “limited assurance,” and that the assurance level would subsequently be raised to “reasonable assurance.” However, in later stages, the plan to raise the assurance level was abandoned, as discussed below.

On February 26, 2025, the European Commission announced a proposal Omnibus I. Its purpose was to simplify certain provisions related to sustainable development introduced by the original CSRD directive and the first iteration of the ESRS standards.

Changes proposed as part of the package Omnibus I are of significant importance to companies, as they concerned both the effective dates of the reporting obligations and the scope of entities that were originally intended to be subject to reporting under the CSRD.

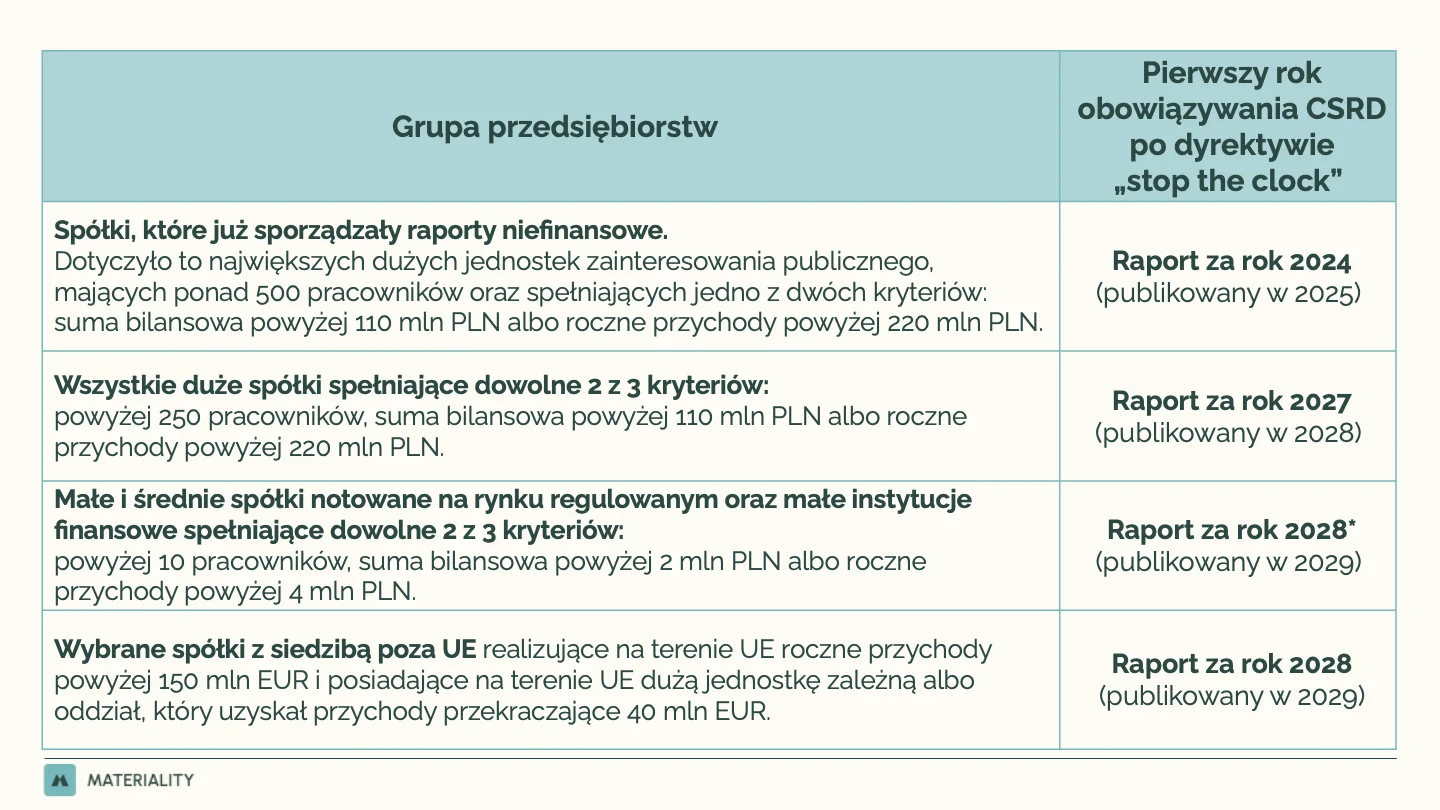

As part of its legislative efforts to simplify sustainable development regulations, the European Commission has begun to signal the need to reduce regulatory burdens and temporarily „pause” the timeline for extending CSRD requirements to specific groups of companies. To this end, even before the final agreement on the changes within the draft Omnibus I, the „stop the clock” directive—that is, Directive (EU) 2025/794—was adopted.

The „stop the clock” directive entered into force on April 17, 2025, and the law implementing it in Poland took effect on August 12, 2025. This measure was intended to allow for smooth work on the Omnibus Package by postponing the application of certain reporting obligations by one or two years.

The next step was to continue working on the package Omnibus I. The amendments to the CSRD were proposed by the European Commission as part of this proposal and were ultimately adopted as Directive (EU) 2026/470. This directive was published in the Official Journal of the European Union on February 26, 2026.

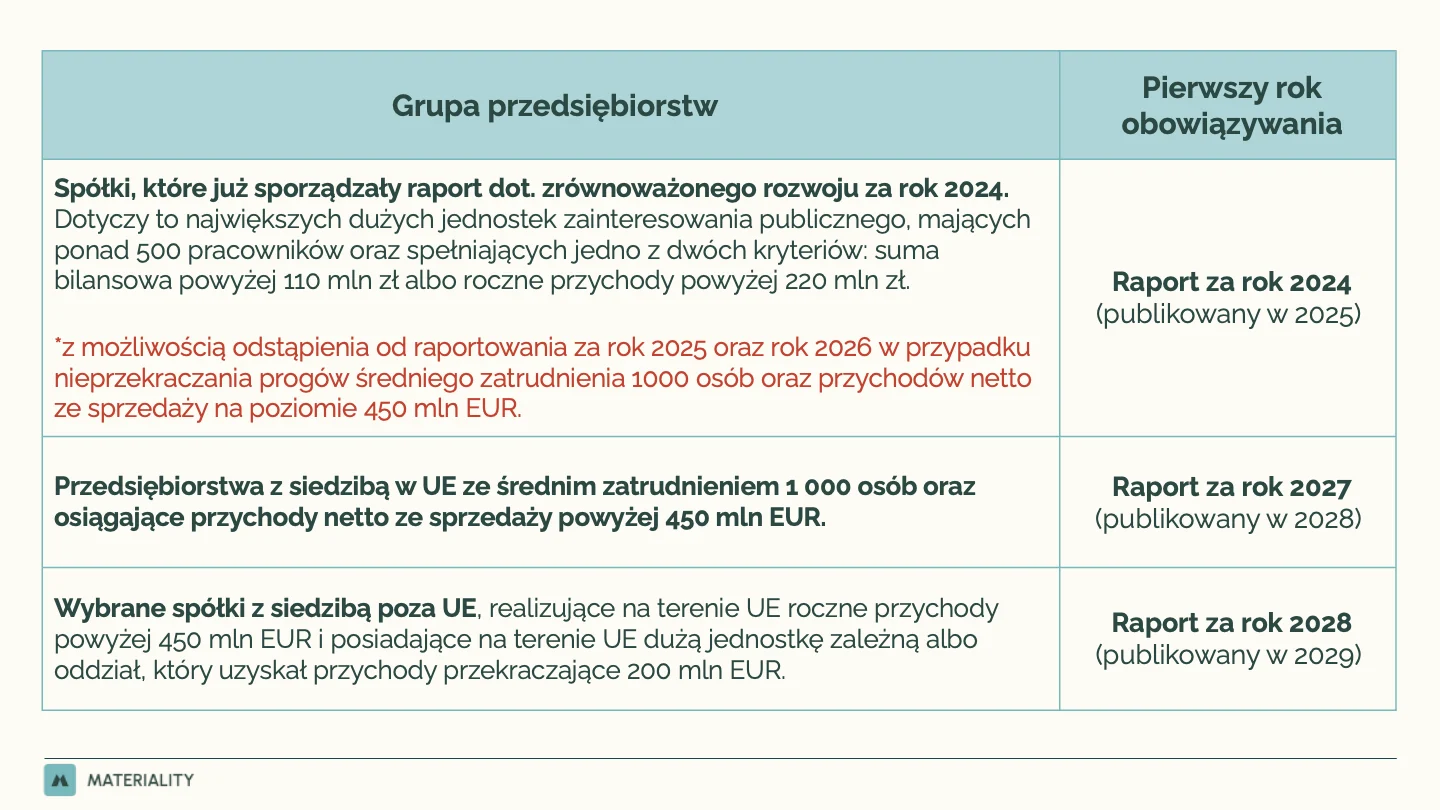

Directive 2026/470 has generally narrowed the scope of entities subject to reporting requirements. It introduced new, higher thresholds and provided for additional exemptions.

These thresholds also apply to corporate groups, with the reporting obligation falling on the parent company.

As a result of the changes introduced by Directive 2026/470, the situation varies among different groups of companies.

The amendments to the CSRD have also expanded the exemption for subsidiaries. A company that meets the criteria establishing a reporting obligation but is part of a corporate group whose parent company prepares a report in accordance with ESRS standards may choose not to prepare its own report. Under the previous regulations, publicly traded companies were not eligible for this exemption. Following the changes, this exemption now also applies to publicly traded companies.

In addition to changing the thresholds and timeline, the Omnibus Directive also introduced other changes regarding sustainability reporting. These changes include the discontinuation of sector-specific reporting standards based on the ESRS and the aforementioned discontinuation of reasonable assurance engagements, in favor of limited assurance engagements,

In Poland, the transposition of Directive 2026/470 is planned to take place in two stages.

Projekt ustawy o zmianie ustawy o rachunkowości, w której implementowane mają zostać zmiany, dostępny jest na stronie Rządowego Centrum Legislacji pod numerem z wykazu prac UC 155.

With regard to sanctions, the Omnibus Directive does not introduce any direct changes to the system of criminal sanctions in Poland. Under current regulations, failure to prepare or certify a sustainability report may result in a fine or a restriction of liberty for the person responsible for its preparation.

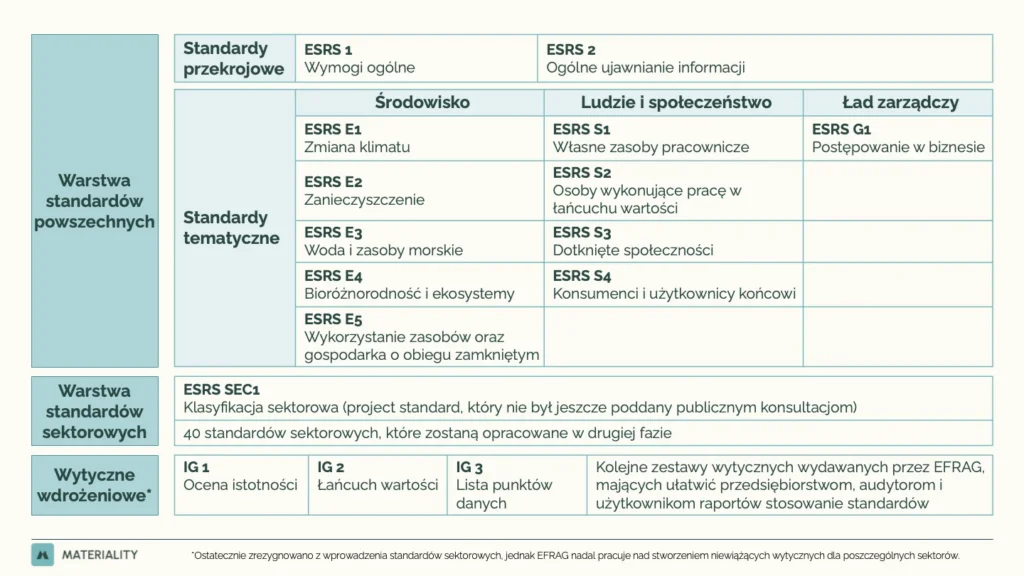

Reports prepared in accordance with the CSRD are drafted in accordance with the European Sustainability Reporting Standards (ESRS).

Projekty standardów przygotowuje dla Komisji Europejskiej EFRAG, czyli Europejska Rada ds. Sprawozdawczości Finansowej. Opracowaniem projektu zajmuje się specjalny zespół roboczy powołany przy EFRAG, czyli PTF ESRS, Project Task Force on European Sustainability Reporting Standards.

This team consisted of Piotr Biernacki, Sustainability Managing Partner at MATERIALITY. He served as co-lead of the subteam that developed draft cross-cutting standards and sets of guidelines. Information about his participation is available here: Piotr Biernacki at EFRAG.

The first ESRS standards were issued by the European Commission in the form of delegated acts. Work is currently underway on simplified ESRS standards. The draft simplified ESRS was publicly announced on December 4, 2025, by EFRAG, and then published by the European Commission as a draft delegated act and subjected to a public consultation that ran from May 6 to June 3, 2026. Trzeciego lipca 2026 r. Komisja Europejska przyjęła zrewidowane, uproszczone ESRS oraz dobrowolny standard raportowania dla mniejszych przedsiębiorstw spoza zakresu CSRD. Przyjęcie przez Komisję nie oznacza jednak zakończenia całej procedury, ponieważ akty delegowane zostały przekazane Parlamentowi Europejskiemu i Radzie do kontroli w ramach tzw. scrutiny period.

On July 31, 2023, the European Commission issued a delegated regulation introducing the first set of ESRS standards. Commission Delegated Regulation (EU) 2023/2772 was published in the Official Journal of the European Union on December 22, 2023.

Delegated Regulation 2023/2772 entered into force and has been applicable since January 1, 2024.

The European system of sustainability reporting standards is based on the ESRS, which define the scope of disclosures required from companies subject to the CSRD.

The changes affected not only the CSRD but also the ESRS standards. On July 11, 2025, the European Commission adopted Delegated Regulation 2025/1416, referred to as the „Quick Fix.” This regulation introduced changes to the first set of ESRS standards.

The goal of „Quick Fix” was to reduce the administrative burden on entities that are already subject to reporting requirements for 2024.

W ramach projektu Omnibus Komisja Europejska zleciła EFRAG przygotowanie projektu uproszczonych standardów ESRS. EFRAG opublikował projekt uproszczonych ESRS, a następnie Komisja Europejska przedstawiła własny projekt aktu delegowanego i przeprowadziła konsultacje publiczne. 3 lipca 2026 r. Komisja Europejska przyjęła zrewidowane standardy ESRS oraz dobrowolny standard raportowania dla mniejszych przedsiębiorstw.

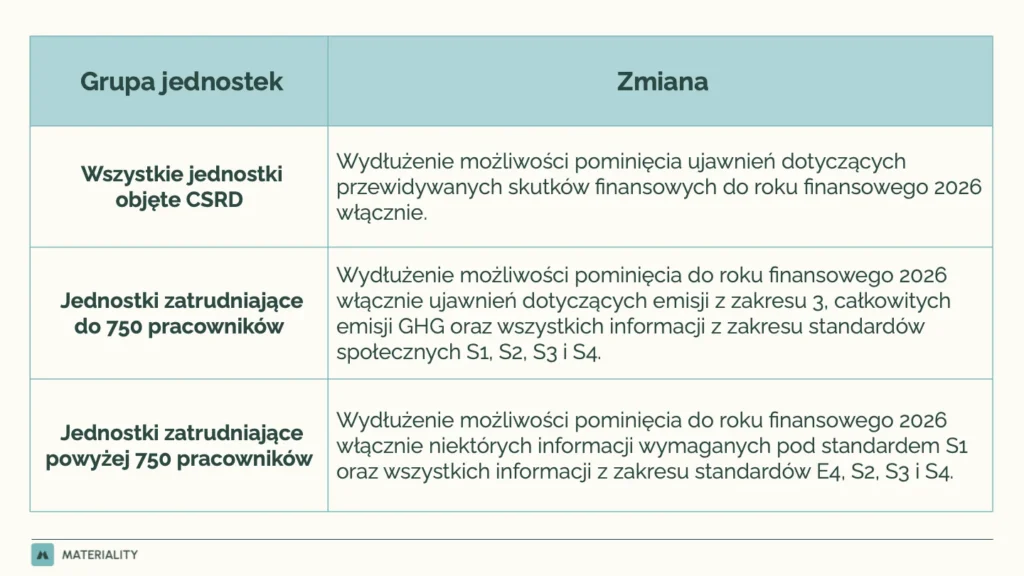

Zrewidowane ESRS mają ograniczyć obciążenia administracyjne, przy jednoczesnym zachowaniu jakości ujawnień. Według komunikatu Komisji z 3 lipca 2026 r. standardy są krótsze i bardziej przejrzyste, wprowadzają dodatkowe elastyczności oraz upraszczają kluczowe procesy. Komisja wskazała również, że liczba obowiązkowych punktów danych została zmniejszona o ponad 60%, a łączna liczba punktów danych o ponad 70%.

Z formalnego punktu widzenia przyjęte przez Komisję akty delegowane zostaną przekazane Parlamentowi Europejskiemu i Radzie do kontroli. Zrewidowane ESRS zaczną obowiązywać dopiero po zakończeniu tego etapu bez zgłoszenia sprzeciwu. Standardowy scrutiny period trwa dwa miesiące i może zostać przedłużony o kolejne dwa miesiące.

Scrutiny period w tym kontekście oznacza okres kontroli aktu delegowanego przez Parlament Europejski i Radę. W tym czasie oba organy mogą przeanalizować przyjęty przez Komisję akt i zgłosić sprzeciw. Jeżeli sprzeciw nie zostanie zgłoszony w przewidzianym terminie, akt delegowany może wejść w życie. Oznacza to, że samo przyjęcie uproszczonych ESRS przez Komisję 3 lipca 2026 r. nie jest jeszcze równoznaczne z ich wejściem w życie.

Zgodnie z przyjętym rozporządzeniem zrewidowane ESRS mogą być stosowane dobrowolnie już do sprawozdań za rok obrotowy 2026. Obowiązkowo będą natomiast stosowane od roku obrotowego 2027, czyli do raportów za 2027 r. publikowanych w 2028 r. W praktyce oznacza to, że jednostki raportujące za 2026 r. mogą zdecydować się na wcześniejsze zastosowanie nowych standardów, ale zasadniczy obowiązek stosowania zrewidowanych ESRS rozpocznie się od raportowania za 2027 r.

Changes to the CSRD and ESRS mean that companies’ reporting obligations may differ from what was originally envisaged in the directive. Some companies have been granted an extension of the deadlines, some may be exempt from mandatory reporting due to the new thresholds, and some will continue to report if they meet the new criteria.

From the perspective of businesses, it is therefore crucial to regularly verify whether they are subject to the reporting requirement, from which year such a requirement may apply, and whether it is possible to take advantage of the exemptions provided for in the regulations. It also remains important to monitor further developments regarding the ESRS, particularly with regard to simplified standards and the practical guidelines for their application.

Regardless of any lack of a reporting obligation, companies may consider voluntarily disclosing information related to sustainability. Such actions can support communication with investors, financial institutions, customers, contractors, and other business partners, especially where market expectations or supply chain requirements go beyond formal legal obligations.

We will guide your company through the entire sustainability reporting process. Learn more about our service and schedule a consultation.

Share